A rolling mean is simply the mean of a certain number of previous periods in a time series.

To calculate the rolling mean for one or more columns in a pandas DataFrame, we can use the following syntax:

df['column_name'].rolling(rolling_window).mean()

This tutorial provides several examples of how to use this function in practice.

Example: Calculate the Rolling Mean in Pandas

Suppose we have the following pandas DataFrame:

import numpy as np import pandas as pd #make this example reproducible np.random.seed(0) #create dataset period = np.arange(1, 101, 1) leads = np.random.uniform(1, 20, 100) sales = 60 + 2*period + np.random.normal(loc=0, scale=.5*period, size=100) df = pd.DataFrame({'period': period, 'leads': leads, 'sales': sales}) #view first 10 rows df.head(10) period leads sales 0 1 11.427457 61.417425 1 2 14.588598 64.900826 2 3 12.452504 66.698494 3 4 11.352780 64.927513 4 5 9.049441 73.720630 5 6 13.271988 77.687668 6 7 9.314157 78.125728 7 8 17.943687 75.280301 8 9 19.309592 73.181613 9 10 8.285389 85.272259

We can use the following syntax to create a new column that contains the rolling mean of ‘sales’ for the previous 5 periods:

#find rolling mean of previous 5 sales periods df['rolling_sales_5'] = df['sales'].rolling(5).mean() #view first 10 rows df.head(10) period leads sales rolling_sales_5 0 1 11.427457 61.417425 NaN 1 2 14.588598 64.900826 NaN 2 3 12.452504 66.698494 NaN 3 4 11.352780 64.927513 NaN 4 5 9.049441 73.720630 66.332978 5 6 13.271988 77.687668 69.587026 6 7 9.314157 78.125728 72.232007 7 8 17.943687 75.280301 73.948368 8 9 19.309592 73.181613 75.599188 9 10 8.285389 85.272259 77.909514

We can manually verify that the rolling mean sales displayed for period 5 is the mean of the previous 5 periods:

Rolling mean at period 5: (61.417+64.900+66.698+64.927+73.720)/5 = 66.33

We can use similar syntax to calculate the rolling mean of multiple columns:

#find rolling mean of previous 5 leads periods df['rolling_leads_5'] = df['leads'].rolling(5).mean() #find rolling mean of previous 5 leads periods df['rolling_sales_5'] = df['sales'].rolling(5).mean() #view first 10 rows df.head(10) period leads sales rolling_sales_5 rolling_leads_5 0 1 11.427457 61.417425 NaN NaN 1 2 14.588598 64.900826 NaN NaN 2 3 12.452504 66.698494 NaN NaN 3 4 11.352780 64.927513 NaN NaN 4 5 9.049441 73.720630 66.332978 11.774156 5 6 13.271988 77.687668 69.587026 12.143062 6 7 9.314157 78.125728 72.232007 11.088174 7 8 17.943687 75.280301 73.948368 12.186411 8 9 19.309592 73.181613 75.599188 13.777773 9 10 8.285389 85.272259 77.909514 13.624963

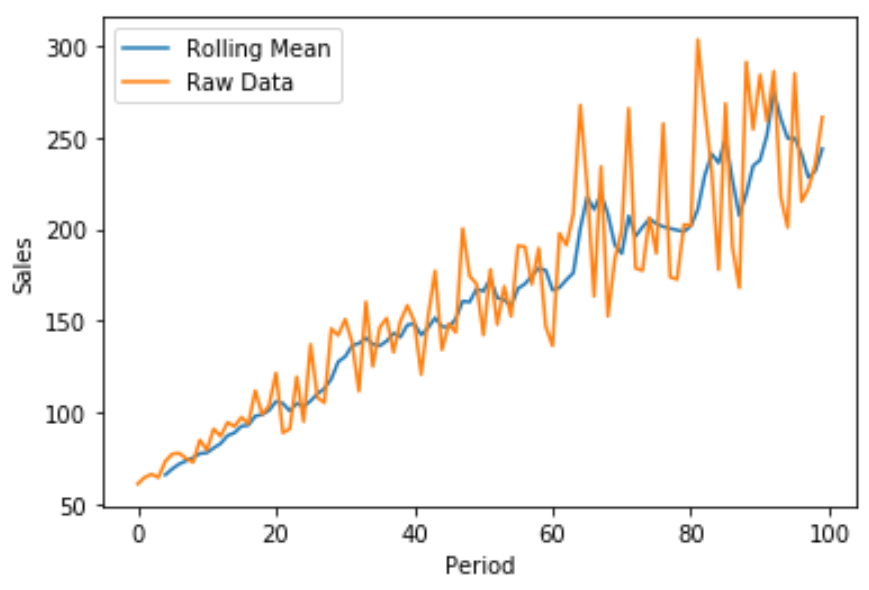

We can also create a quick line plot using Matplotlib to visualize the raw sales compared to the rolling mean of sales:

import matplotlib.pyplot as plt

plt.plot(df['rolling_sales_5'], label='Rolling Mean')

plt.plot(df['sales'], label='Raw Data')

plt.legend()

plt.ylabel('Sales')

plt.xlabel('Period')

plt.show()

The blue line displays the 5-period rolling mean of sales and the orange line displays the raw sales data.

Additional Resources

The following tutorials explain how to perform other common tasks in pandas:

How to Calculate Rolling Correlation in Pandas

How to Calculate the Mean of Columns in Pandas